What Most Agents Don’t Explain

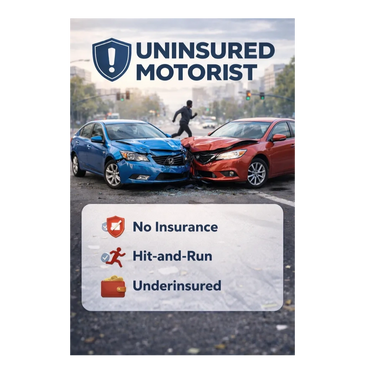

UNINSURED MOTORIST

ROOFS- REPLACEMENT COST VS ACTUAL CASH VALUE

UNINSURED MOTORIST

What does Uninsured Motorist (UM) coverage cover?

Uninsured Motorist (UM) coverage helps pay for your injuries and damages if you’re hit by a driver who:

- Has no insurance

- Doesn’t have enough insurance (underinsured)

- Leaves the scene (hit-and-run)

It can help cover: - Medical bills

- Lost wages

- Pain and suffering

- In some cases, damage to your vehicle (depending on your state and policy) NOT IN OKLAHOMA!

Think of it as protection for you and your passengers when the other driver can’t pay.

What does Uninsured Motorist NOT cover?

UM coverage does not cover:

- Damage to your own vehicle!!!!

LIABILITY LIMITS

ROOFS- REPLACEMENT COST VS ACTUAL CASH VALUE

UNINSURED MOTORIST

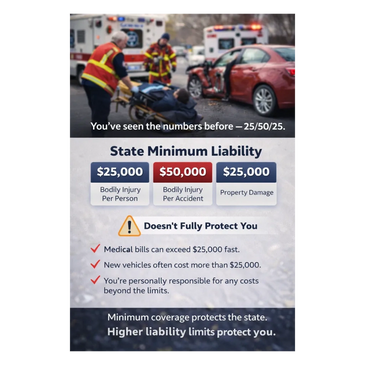

You’ve seen the numbers before — 25/50/25

That’s state minimum liability in many states:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $25,000 property damage

It keeps you legal. It does not fully protect you.

- Medical bills can exceed $25,000 fast.

- New vehicles often cost more than $25,000.

- If damages go beyond your limits, you’re personally responsible for the difference.

That can mean lawsuits, wage garnishment, or paying out of pocket.

Increasing limits to something like 100/300/100 is usually far more affordable than people think — and it protects your home, savings, and future income.

Minimum coverage protects the state.

Higher liability limits protect you.

ROOFS- REPLACEMENT COST VS ACTUAL CASH VALUE

ROOFS- REPLACEMENT COST VS ACTUAL CASH VALUE

ROOFS- REPLACEMENT COST VS ACTUAL CASH VALUE

⚠️ Roof Coverage: This Is Where Claims Get Painful

Most homeowners don’t realize this until it’s too late.

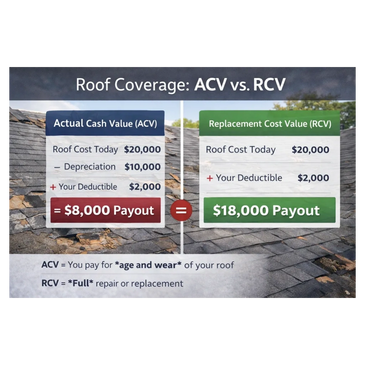

If your roof costs $20,000 to replace and you have a $2,000 deductible…

🔴 ACV (Actual Cash Value)

Insurance subtracts depreciation for age and wear.

$20,000 (cost to replace)

– $10,000 depreciation

– $2,000 deductible

👉 You receive $8,000.

👉 You come up with $12,000 out of pocket.

🟢 RCV (Replacement Cost Value)

Insurance pays full replacement cost minus your deductible.

$20,000 (cost to replace)

– $2,000 deductible

👉 You receive $18,000.

👉 You pay $2,000.

Huge difference.

The Reality

ACV keeps premiums lower.

RCV keeps your savings intact.

ACV pays what your roof is worth.

RCV pays what it costs to replace it.

** You want RCV

Ask me how long your roof will be covered at RCV.